The Boeing 737 Problem: Why Nuclear Energy Needs FAA-Style Type Certification

When the FAA certifies a new aircraft design, it certifies the design — once. Every subsequent aircraft built to that design rolls off the production line with the full benefit of that upfront regulatory work. An airline buying its fifteenth 737 MAX does not ask Boeing to re-engineer the wing. The regulator does not re-litigate the aerodynamics. The safety case transfers. Production scales. Costs fall.

This seems obvious. In aviation, it is. In nuclear energy in the United States, it is not. Each site requires a separate licensing process even for already-approved reactor designs — and that gap is costing the country a generation of clean, reliable power.

What Type Certification Actually Means

Under the FAA framework, type certification is the approval of a specific aircraft design against applicable safety standards. Once a design clears that threshold, the manufacturer receives a production certificate to build duplicates of it at scale. Each individual aircraft still requires its own airworthiness certificate before it can fly, but that certificate simply confirms that the aircraft was built to the certified type design — it does not re-examine the underlying physics.

The result is a tiered, efficient system. Heavy regulatory scrutiny is applied once, at the design stage, where it is most valuable. Subsequent builds are validated, not re-adjudicated.

The Nuclear Analogy — and Where It Breaks Down

The NRC’s existing framework under 10 CFR Part 52 includes a design certification process that, on its face, resembles type certification. A reactor designer submits an application, the NRC reviews it, and if approved, subsequent applicants can reference the certified design in their Combined Construction and Operating License (COL) applications without relitigating the core safety case.

In theory, this should work similarly to the FAA model. In practice, it has not.

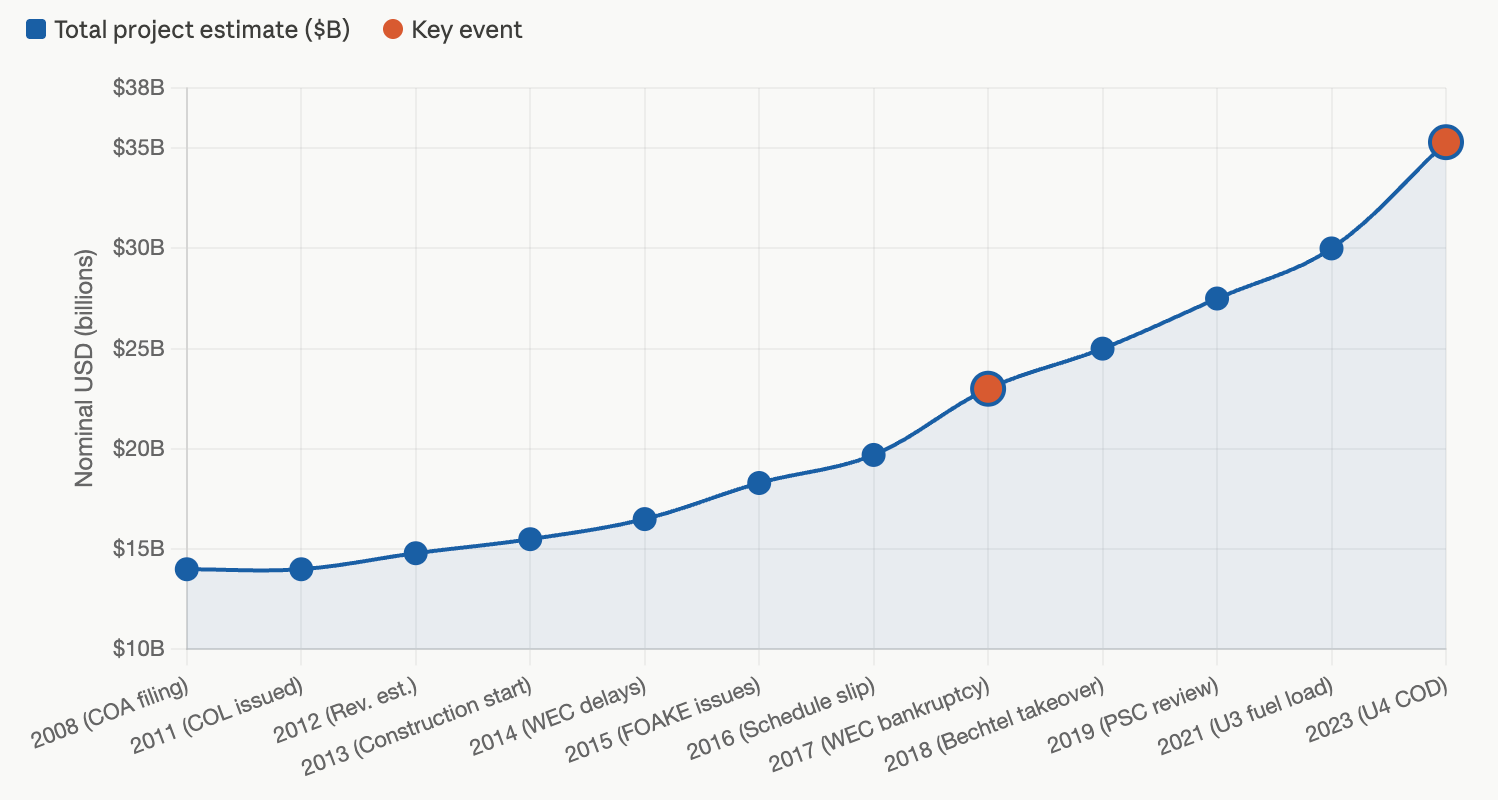

The AP1000 — Westinghouse’s Generation III+ pressurized water reactor, the most advanced large commercial reactor design currently certified in the United States — illustrates the problem with precision. Westinghouse submitted the AP1000 standard design certification application to the NRC in March 2002 and received approval in 2006. That certification was subsequently amended, with the latest version, Revision 19, approved in 2011. Yet when Southern Company went to build Vogtle Units 3 and 4 using that certified design, it still filed over 180 license amendment requests by the time the project was complete.

Read that number again: 180 site-specific departures from a supposedly standardized, pre-certified design. Each one required NRC staff review. Each one added time, cost, and uncertainty to a financing structure that was already stretched thin.

The Fukushima disaster in 2011 added a further complication. A 19th revision to the AP1000 Design Certification was written, which effectively included a complete redesign of the containment building. This change was mandated after engineering contracts were already signed and manufacturing had begun on long-lead-time components. The result was a construction halt — a mid-project design re-opening that would be unthinkable in any mature industrial sector.

The Financial Consequences Are Not Abstract

For capital markets professionals, what matters is not the regulatory philosophy — it is the cost of capital. And the current regime has a direct, quantifiable impact on financing economics.

When the state of Georgia approved the Vogtle project in 2009, the expectation was that Units 3 and 4 would cost $14 billion and begin commercial operations in 2016 and 2017. The eventual all-in cost for the two units exceeded $30 billion — more than double the original estimate — with Unit 3 coming online in July 2023 and Unit 4 in April 2024, roughly seven years behind the original schedule. Of course, a significant contributing factor was that the previously-approved design had to be completely re-engineered to comply with the new aircraft impact assessment rule, after construction had already started at Vogtle 3 & 4 and V. C. Summer 2 & 3 (the latter of which was never completed and remains half-built).

Sources: Georgia Power Company, Vogtle Units 3 & 4 Construction Monitoring Reports, Georgia Public Service Commission Dockets 29849 and 40339 (2012–2023); Southern Company, Annual Reports and 10-K filings (2012–2023); U.S. GAO, Nuclear Power: NRC’s Oversight of New Reactor Licensing (GAO-19-204, 2019). All figures are in nominal dollars. 2012 estimate reflects Southern Company’s revised projection after construction permit. “Final” reflects SNC-Lavalin/Bechtel completion estimate at Unit 4 COD (July 2023).

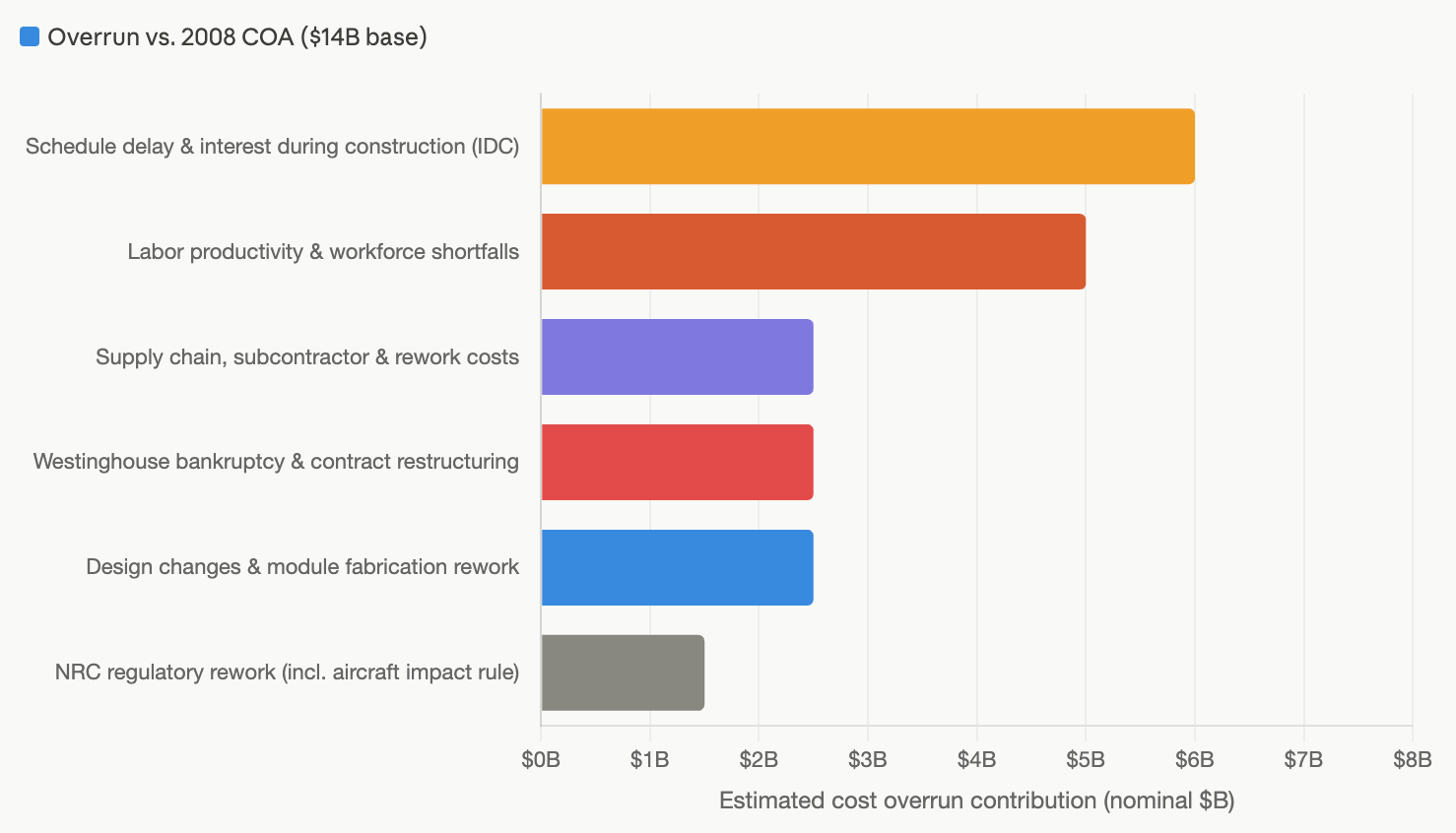

The cost factor decomposition in Figure 2 represents the author's analysis of publicly available primary sources and should not be read as an audited accounting of Vogtle Units 3 & 4 construction expenditures. Total project cost estimates at each milestone are drawn from Georgia Power's semi-annual Construction Monitoring Reports filed with the Georgia Public Service Commission (Dockets 29849 and 40339). Causal attribution across factors draws additionally on: the Westinghouse Electric Company Chapter 11 disclosure statement and settlement agreements (Bankr. S.D.N.Y. No. 17-10751, 2017–2018); NRC Confirmatory Action Letters and design change inspection reports accessed through the NRC’s ADAMS public document system; and DOE Loan Programs Office monitoring summaries for the Title XVII loan guarantee portfolio. Attribution of costs to the aircraft impact design requirement (10 CFR 50.150) relies on NRC design change notices and is presented as a component of the broader “design changes” category in Georgia Power filings; no standalone audited figure for this line item is publicly available. Interest during construction (IDC) is estimated based on reported schedule slippage against the original 2016–2017 commercial operation date targets and Southern Company’s disclosed weighted average cost of capital for rate-regulated assets. All figures are nominal USD. For comparative cost escalation methodology, see Buongiorno et al., The Future of Nuclear Energy in a Carbon-Constrained World (MIT Energy Initiative, 2018), ch. 4; and Lovering, Yip & Nordhaus, “Historical construction costs of global nuclear power reactors,” Energy Policy 91 (2016): 371–382.

Regulatory indeterminacy was not the only culprit. Vogtle began construction with an incomplete design, an immature supply chain, and an untrained workforce. But the feedback loop between design instability and regulatory re-opening is inseparable from those other failures. Mid-construction design changes require new regulatory review. New regulatory review extends the timeline. Timeline extension compounds financing costs on a project with billions of dollars of in-process capital. Westinghouse’s bankruptcy in 2017 was the downstream consequence.

The lesson for structured finance is clear: you cannot underwrite a project where the design is legally re-openable mid-construction. The risk profile is unboundable. No reasonable credit model can assign a probability distribution to “the regulator may require us to redesign the containment building after steel has been erected.”

The NOAK Promise — and What It Requires

Here is where the policy and the economics converge.

The data from China’s second series of AP1000 builds — using the same base design, with accumulated experience — is instructive. The second series of Chinese AP1000 projects achieved a 48% reduction in average duration from first nuclear concrete to milestone completion and a 42% reduction in average duration between milestones compared to the first series. Variance also fell sharply, with schedule predictability improving by roughly half.

MIT’s Center for Advanced Nuclear Energy Systems has modeled what these learning-curve dynamics imply for U.S. nth-of-a-kind (NOAK) costs. In a moderate scenario, the second, third, and fourth two-unit AP1000 plants are projected to have an overnight capital cost of $10,000/kWe, $7,800/kWe, and $6,200/kWe, and be built in 7 years, 6 years, and 5.5 years, respectively. At the fourth plant, that implies an LCOE that begins to compete with other firm clean energy sources without sustained subsidy.

But this cost reduction curve only materializes under one condition: the design stays locked. Every mid-project regulatory re-opening, every site-specific amendment, every design change review resets the learning clock. The Chinese builds achieved their schedule reductions precisely because they were building the same thing, repeatedly, with accumulated institutional knowledge and a stable regulatory baseline. The U.S. framework, as currently structured, undermines that dynamic by preserving too many avenues for design reopening.

What True Type Certification Would Look Like

A properly structured type certification regime for nuclear reactors would borrow the core logic of the FAA model while accounting for the genuine differences in risk profile and regulatory context.

The essential elements are three:

First, binding design lock. Once a reactor design receives type certification, that design is frozen for construction purposes. Site-specific adaptations — seismic inputs, grid interconnection, cooling water source — are addressed through a defined interface specification that is resolved at permitting, not re-litigated during construction. The equivalent of an airworthiness certificate confirms that the plant was built to the certified design; it does not re-examine whether the passive safety systems work.

Second, safety-significance gating. Not every deviation from a certified design warrants full regulatory review. The FAA distinguishes between changes that require a new type certificate, an amended type certificate, or simply a notification, based on the significance of the change. Nuclear regulation should apply the same logic formally and consistently, with a clear, pre-defined threshold above which re-review is triggered and below which it is not. This is the principle behind the NRC’s Tier 1/Tier 2 distinction under Part 52, but that framework has proven porous in practice.

Third, prospective, not retrospective, safety standards. The mid-construction Revision 19 redesign at Vogtle — triggered by a post-Fukushima NRC mandate — represents the single most destructive feature of the current regime from a financing perspective. A genuine type certification framework would establish that the design is certified against the standards in force at the time of certification, with a defined and limited process for post-certification safety findings. Changes to safety requirements applied after construction commences must be treated as government-caused project disruptions, with defined compensation mechanisms, not simply absorbed as project risk by investors.

The Legislative and Regulatory Landscape

It would be wrong to suggest that policymakers are unaware of these problems. The ADVANCE Act of 2024 was passed with bipartisan support and signed into law in July 2024, requiring the NRC to take a number of actions, particularly in the areas of licensing of new reactors and fuels, while maintaining the NRC’s core safety and security mission.

Executive Order 14300 went further. The order calls for binding licensing deadlines: no more than eighteen months for decisions on new reactor applications and no more than twelve months for license renewals, with NRC fee recovery capped to prevent prolonged processes from inflating costs.

The NRC has also recently extended the AP1000’s design certification. The NRC extended the design certification for Westinghouse’s AP1000 until February 2046, as announced on August 27, 2025, reinforcing the AP1000’s role as a cornerstone of advanced nuclear technology.

And the new Part 53 framework — a proposed technology-inclusive, risk-informed licensing pathway for advanced reactors — represents genuine progress on the regulatory architecture, fundamentally reorganizing the reactor licensing framework around risk-informed regulation, in which risk insights derived from probabilistic risk assessment play a central role in safety decisions.

These are meaningful steps. But they do not yet deliver what the capital markets need: a credible, legally binding commitment that a certified design will not be re-opened mid-construction as a matter of routine regulatory discretion. The licensing timeline reforms address how long the front-end review takes. What is still missing is a mechanism that makes the back-end — the construction phase itself — financially underwitable.

The Capital Markets Case

The argument for type certification reform is often framed in terms of industrial policy or energy security. Those arguments are correct, but they are not the arguments that move project finance committees.

The capital markets case is simpler: standardized, legally locked designs reduce the variance of project outcomes. Reduced variance is the precondition for debt financing at scale. Debt financing at scale is the precondition for levelized costs that can compete without perpetual government subsidy. And competitive levelized costs are the only durable path to a nuclear renaissance that outlasts any particular administration’s enthusiasm for the technology.

The AP1000 pipeline is real and growing. Twenty-four more AP1000s are currently being planned, with six in India, nine in Ukraine, three in Poland, two in Bulgaria, and four in the United States. In 2025, Fermi America signed an agreement with Doosan Enerbility to deploy four AP1000s as part of a data center development in Amarillo, Texas. V.C. Summer is being revisited by Santee Cooper and Brookfield. Turkey Point Units 6 and 7 hold an existing COL. William States Lee in North Carolina is in active development.

The pipeline is there. The design is proven. The learning curve is real. What is missing is the regulatory architecture that allows capital to flow at the scale and cost the buildout requires.

Type certification reform is not a deregulatory argument — it is a structural finance argument. The question is not whether nuclear is safe. The AP1000’s passive safety systems, its operating record in China, and its NRC design certification all answer that question. The question is whether the regulatory framework is structured in a way that allows investors to price the risk of building one. Right now, the honest answer is: not reliably.

Fixing that is the work of the next decade. The tools exist. The analogy is proven. The only thing missing is the political will to apply it.

The author is a structured finance attorney focusing on energy and capital markets transactions. The views expressed are the author’s own and do not reflect those of his employer.